The ongoing conflict in the Middle East is no longer a regional issue. Its effects are now embedded across global supply chains, reshaping how goods move, how much they cost, and increasingly how their environmental impact is measured.

• 15 days added to Asia - Europe ocean transit times

• Up to 10% effective capacity reduction across ocean networks

• Air freight facing longer routings and reduced usable capacity

• Sustained fuel volatility as transport cost increases

• 30-40% increase in emissions on some diverted routes

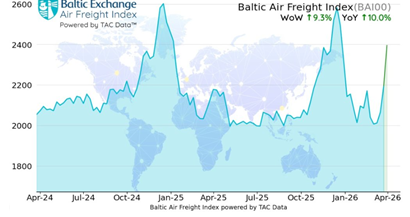

AIR FREIGHT

Airfreight rates are heading back towards peak-season levels as the disruption caused by the conflict in the Middle East and rising fuel prices continue to put pressure on the cargo market.

While ocean networks have been operating inefficiently for some time, air freight is now experiencing the fastest-moving disruption linked to the Middle East escalation.

As the Middle East represents a major global air cargo transit region, airspace restrictions, operational risk, and instability across key Gulf hubs are therefore having an outsized impact on global uplift.

This is driving:

• Longer, less direct routings, increasing flight distances and fuel burn.

• Reduced effective belly hold capacity, as passenger schedules change or are withdrawn, and increased fuel weight for longer routings reduces cargo capacity.

• Spill over demand from ocean freight, as some shippers move time-sensitive cargo to air to protect supply continuity.

• Greater reliance on indirect and multimodal routings, as traditional hubs become less predictable, despite some return of capacity on some routes.

The shipping disruptions through the Strait of Hormuz are also increasingly threatening to disrupt the global aviation industry, not just because major international airports in the Middle East were forced to close or operate at limited capacity due to drone and missile strikes. According to estimates, around 20% of the world’s jet fuel supply normally passes through the Strait of Hormuz.

Fuel expenses are typically the second-highest cost factor for airlines after labour-related costs, usually accounting for around a fifth to a quarter of an airline’s operating costs.

SEA FREIGHT

Extended diversions around the Cape of Good Hope have been in place since late 2023, adding 15+ days to Asia–Europe transit times compared to historic Suez routings.

These longer voyages had already reduced network efficiency before the current escalation.

What has changed is the degree of pressure now being applied to an already stretched system.

From a global ocean freight perspective, this is resulting in:

• Effective capacity reduction of approximately 6–10%, as longer round voyages absorb vessel time that would otherwise be available elsewhere.

• Increased schedule volatility, caused by disruption to key Middle East shipping corridors, is creating wider network instability. Vessel diversions, congestion at alternative ports and longer transit times are increasing schedule volatility globally, with blank sailings, port omissions and vessel bunching becoming more frequent.

• Upward pressure on costs, due to higher bunker consumption resulting from longer vessel routings, schedule recovery measures and congestion-related delays, alongside elevated insurance exposure and contingency planning requirements.

As a result, carriers are increasingly applying surcharges with shorter rate validity periods.

• Equipment and space imbalances, particularly in Asia, are increasing rollover risk even where nominal capacity exists.

These impacts are global rather than regional, with capacity absorbed on Asia–Europe services continuing to create knock-on congestion and cost pressure across

Transpacific and regional trades.

The world of trade is stuck in a sea of costly red stop signs and detours.

Multiple sources of trade data are showing the significant impact of the U.S.-Israel war on Iran and how it is going to continue to get worse before it gets better.

Over 80 per cent of the world’s 454 ports mapped are deemed in critical status, 60-70 per cent are severely congested, and 45-59% are considered highly congested.

To circumvent the container contagion, ocean carriers are making the logical decision to suspend services, update their services on other routes, and charge more. The longer routes burn more fuel, and that fuel is way more expensive. Slow steaming is also used, but it adds time to an already behind schedule.

FUEL

While countries in Asia remain among the worst affected by intensifying fuel shortages, supply disruptions are also starting to spread to other parts of the world, with a growing number of governments in Europe announcing emergency measures to protect domestic fuel supplies and prevent panic-buying at petrol stations.

With shipping through the Strait of Hormuz largely halted, the number of countries affected by fuel shortages is likely to increase further in the coming weeks if no resolution to the conflict is found.

Alongside ocean and air disruption, the conflict is exerting sustained pressure on global fuel markets, with diesel and jet fuel prices rising sharply and remaining volatile. Heightened risk around the Strait of Hormuz has introduced a persistent “war premium” into energy pricing, with consequences across inland transport.

For road freight globally, this is resulting in:

• Rising diesel costs across the globe.

• More frequent fuel surcharge adjustments, with shorter review cycles becoming common.

• Upward pressure on domestic and cross-border trucking rates, particularly where fuel represents a high proportion of total cost.

• Increased cost sensitivity on inland legs, including port drayage, cross-border moves and final mile delivery.