AIR FREIGHT

Major trades out of Hong Kong and Frankfurt saw airfreight rates stabilize in August after months of declines [see dashboard below].

- Rates from Hong Kong to Europe in August increased compared to July. The last time rates didn’t decline compared with the previous month on the trade was August 2022.

Rates on the trade are down from a year ago but are up compared to the level recorded in August 2019.

The improvements in rates on the trade in August compared with July mirrors usual seasonal patterns when prices tend to be fairly flat over the summer months.

- The latest figures from the Baltic Exchange Airfreight Index (BAI) show that average prices on services from Hong Kong to North America increased in July.

It is only the second time rates on the route have increased compared with the preceding month in the last 12 months, the others being in December and March.

However, prices remain above the pre-Covid 2019 level.

Yet, as they come off the back of a period of declines, there might be a signal that the market may have reached the bottom: TAC Index said in its weekly market report that strong e-commerce business out of southern China continued to keep rates edging up from that region.

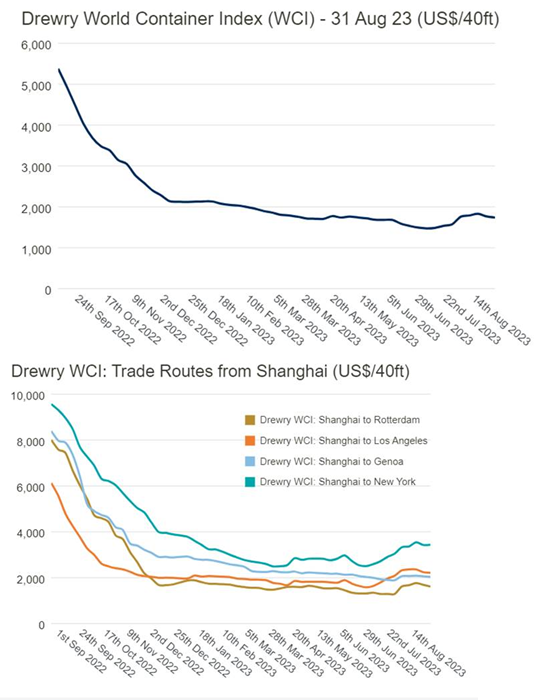

SEA FREIGHT

Global maritime rates continued to fall through August.

Looking at the top 8 trade lanes around the world, the average rate of change for prices month-over-month was down 2.4%.

As an example, all the Shanghai routes (to Europe, US East Coast, etc.) were down between 3.4% and 5.1% month-over-month.

To keep it all in perspective, one must compare rates to where they were prior to the pandemic, and most routes are still sharply elevated versus August of 2019.

And this is part of the global inflation challenge that the world continues to work through.

The average across the 8 primary trade lanes showed that rates today are still 25.6% higher than they were prior to the pandemic.

Based on historic growth rates, prices are still 10% higher than they should be (based on the long-term growth trend).

Carriers are pulling capacity out of the market and the backup at the Panama Canal has also worked to pull capacity out of the industry.

In a nutshell:

RATES WENT DOWN BECAUSE OF CAPACITY INCREASE, BUT DUE TO HIGHER NUMBER OF BLANK SAILINGS DURING THE SUMMER, RATES STARTED TO INCREASE AGAIN

Source Drewry

PANAMA CANAL SITUATION

Panama Canal’s operations have been impacted by a water shortage caused by insufficient rainfall in the past year.

As a result, the Panama Canal Authority has put in place a water restriction for 10 months, reducing the daily number of allowed transit vessels from 36 to 32.

Additional lower water level restrictions imposed by the PCA require vessels to be 40% lighter, requiring more vessels to move the same amount of product.

The resulting congestion and delays are currently mainly affecting tankers, LPG, and bulk container vessels, with delays of up to 2 weeks.

Container ships, alongside cruise ships are given priority, with minimum impact on global supply chain clients thus far.

Data shows that despite the challenges, the situation is still under control and it is not yet to be considered a crisis.

Container vessel traffic using the Panama canal has seen some delays and added costs but the impact so far has been minimal.

Container ships have not seen major disruptions with almost unvaried average waiting times, at less than a day.

TRUCKING SITUATION IN THE USA

LTL carrier Yellow Freight officially shut down operations, creating the largest trucking bankruptcy in history.

The question for most is, what will happen in the LTL sector now?

Analysis studying the closure of Consolidated Freightways in 2001 showed that prices in the LTL sector increased by 4-6% over the 12 months that followed.

Analysts today believe that LTL prices could increase an average of 6% over the next year, depending on how quickly the US emerges out of its freight slowdown.