AIR FREIGHT

The latest air freight statistics confirm the ongoing stabilization of the market, both in terms of volumes and rates: according to recent data released by the International Air Transport Association (IATA), global air cargo markets showed a continued, but slower, decline against the previous year’s demand performance.

Overall, the second quarter of 2023 ended with improved volumes compared to the first quarter.

Air cargo demand remains soft for general cargo due to being in a traditionally slack season.

This is expected to continue into the next month, prior to the anticipated improvement towards the end of the third quarter.

Global air freight tonnages decreased in June by 4% compared to June 2022, a decline that decelerates month after month since it was -6% in May and -10% in April.

Average airfreight rates across the world are also

As for the Baltic Airfreight Index (BAI), the drop in the global index reached 49% in June, over one year.

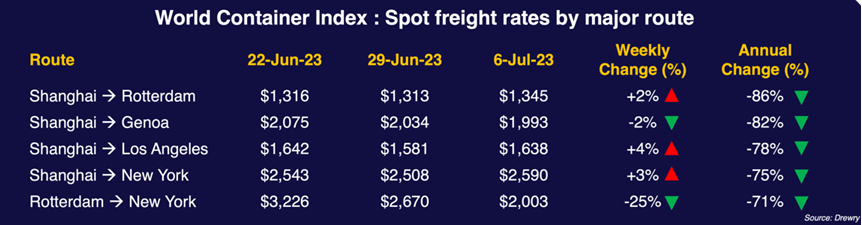

SEA FREIGHT

The global shipping industry is responsible for 90% of world trade.

And approximately 40% of total containerized trade lies on the main East-West routes—those between Asia, Europe, and the United States.

These numbers showcase the pivotal role logistics plays within today’s global economy.

As the second half of the year has started, the effects of moderate global trade continue to be evident.

Although ocean freight volumes have been lower in recent months due to the changed global market situation, there are still some trade lanes showing stronger capacity utilization.

This is influenced by several factors, such as the

Maritime transport is, therefore at a crossroads.

First of all, because no peak season is coming.

Besides, the companies have created a situation of historical overcapacity (the maritime transport capacity has increased by 40% over one year on the Asia-Europe axis.) while engaging in a tariff war.

For them, the situation is becoming increasingly worrying: they are currently losing between 500 and 700 USD/FEU on Asia-Europe trades, and no “cash cow” trade is there to compensate.

Spot rates have indeed collapsed on the Transatlantic trade lane.

Finally, the companies are also facing an increase of around 1/3 in the costs of managing their ships, modernized and renewed thanks to the profits accumulated during the post-Covid rebound.

The race for low rates is probably over.

The announcement of GRI (General Rate Increase) in August by Maersk and CMA CGM will undoubtedly be followed by a wave of blank sailings, to support this voluntary rate increase.